To see the original publication of this article visit S&P Global Market Intelligence.

After testing the M&A waters, Texas National Bank instead turned to digital banking to drive organic growth.

Texas National is set to launch a digital banking platform called Bankers Lender in April, built upon a so-called sidecar core banking system developed by Data Center Inc., the companies announced March 15. The bank invested about $100,000 in the new core banking system that will run alongside its current core, which it has used for 20 years for its community banking business.

The decision came after Texas National held talks regarding a potential branch acquisition and a whole bank acquisition over the past 12 months, said Mike Fernandez, president and CEO of Texas National Bank. It was very interested in pursuing the branch acquisition to add new markets, but the transaction took longer than the parties anticipated. "So through that process, we thought to ourselves, we can't be beholden to the decisions of other things that are outside of our control," Fernandez said.

Break the bottleneck of organic growth

Like many smaller institutions, Texas National faces challenges in a rapidly evolving banking industry. Banks across the country are trying to figure out the best way to grow and address their technology issues, especially as they face competition from upstart digital players.

Many have pursued inorganic growth as evidenced by the industry's decadeslong consolidation run. The activity accelerated in 2021 with the total value of M&A surging to a 15-year high. Leveraging greater economies of scale to improve the efficiency of technology has often been cited as a driver of large bank M&A deals.

However, some, like Texas National, find that the traditional ways of expansion via a bank or branch acquisition or a de novo market entry could be extremely costly endeavors, Fernandez said. Texas National estimates that a bank M&A for an organization of its size could be a seven-figure investment, and it will face the risks of merging cultures, losing customers, and converting the core systems.

"We were hesitant to consider paying a premium and branching in that way ... when we can spend $100,000 and have a more rewarding outcome," Fernandez said.

A de novo also brings risks. Along with the cost of overheads, a successful market entry depends on finding the right talent, Fernandez said. The family-owned bank had $171 million in total assets as of the end of 2021 and operates in two markets in Texas — Sweetwater and Tuscola — where the population is about 10,000 and 750, respectively. With limited economic and population growth and recent declines in loans, the bank operates at a very low loan-to-deposit ratio of about 20%, Fernandez said.

Modern cores advantage banks

For regional and community banks lacking internal technology resources and talent, modern cores enable them to add digital interfaces to reach customers and integrate with third-party fintech applications. It helps banks level the playing field with fintechs that have been increasingly encroaching onto their turf. Banks use core banking systems to issue cards; move money among consumers, merchants, other banks and the Federal Reserve; and ensure compliance in every step from account opening to record-keeping.

Legacy core banking systems — some of which are supported by technology that dates back to the 1970s, according to a SoFi Technologies Inc. investor presentation — are often viewed as reliable but chunky and were designed to serve the bank itself with the goal of operational stability and compliance.

As a result, the bank's ledgering process, an essential function of a core system to record money movement transactions, could get messy if a bank uses legacy core systems to run fintechs on the side, said Dave Mayo, CEO of banking data and insights company FedFis. Sidecar cores aim to tackle this issue to allow banks to better organize business outside of their core lines, such as digital banking and banking-as-a-service.

A bank equipped with technology will have an edge that the majority of fintechs do not — the charter. Fintechs are increasingly attracted to owning a charter through bank acquisitions. Without a charter, a fintech has to work with sponsor banks, but more issues around the demanding and costly integration efforts have surfaced in recent years. Some fintechs view it as a less profitable model that carries regulatory burdens, especially for those that have grown out of the stage of building the initial customer base.

While a bank charter application costs fintechs years and millions of dollars, a smaller bank can take advantage of its charter by stepping into fintech arenas. Data Center Inc., known as DCI, sees a busy pipeline of banks planning to launch digital branches and banking-as-a-service, said Tanna Faulkner, DCI's senior vice president of digital channels and sales. With digital branches, banks' growth will no longer be constrained by geographic locations, and with banking-as-a-service, they can embed their card issuing and payments capabilities in various applications for fintechs and nonfinancial enterprises.

More innovation to come

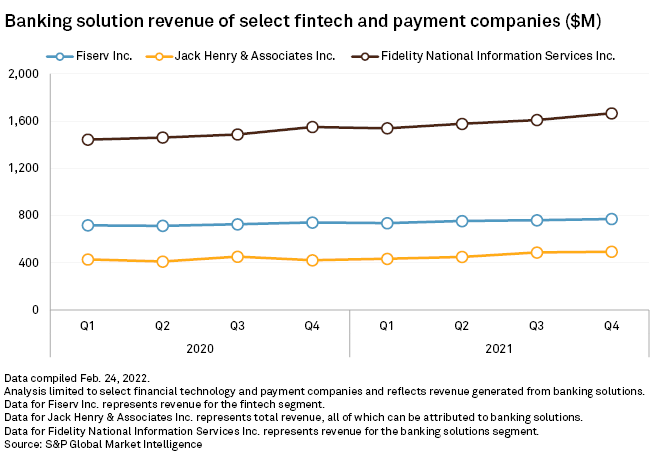

Historically the core banking market has been dominated by Fiserv Inc., Fidelity National Information Services Inc. and Jack Henry & Associates Inc. FedFis estimated that Fiserv holds 40% of the core banking market share as of the first quarter of 2022, while Jack Henry holds 18% and FIS holds 16%.

While the core banking vendors reported a busy fourth quarter facilitating system conversions for their customers who were making acquisitions or being acquired, the market share overall appeared to stand still. The declining number of banks does not necessarily mean a shrinking total addressable market because they are reinventing themselves with other sources of revenue, said Ruby Walia, senior adviser for digital banking at Mobiquity.

The momentum of innovation will continue as those serving the market are reshaping.

In a Feb. 9 earnings call, Jack Henry executives revealed a cloud-native core banking platform in the works, which enables easier integration with various fintech applications. On Feb. 7, Fiserv Inc. announced plans to acquire the remaining ownership of cloud-native banking solutions provider Finxact Inc. for approximately $650 million. On March 3, SoFi Technologies Inc. closed its acquisition of Argentina-based Technisys SA, adding core banking capabilities on top of a payments processing subsidiary, Galileo Processing Inc., and a chartered bank, SoFi Bank NA.

SoFi hopes to offer a streamlined core banking product for banks, since banks often end up having to use different cores and ledgers for the same customer. SoFi uses two separate third-party core banking providers. But over time, it will be using Technisys for SoFi Money, its cash management account, as well as SoFi Credit Card, said SoFi's CFO, Christopher Lapointe.

Other emerging fintechs have made inroads into banking software, such as Mambu GmbH, nCino Inc. and Q2 Holdings Inc. In 2021, JPMorgan Chase & Co. replaced its retail core banking system in the U.S. with that provided by London-based Thought Machine Inc. For small community banks like Texas National, the availability of technology means more opportunities to experiment with growth venues.

"There's a lot of opportunity for us to bring some business to the bank and improve that top-line revenue," Texas National's Fernandez said. "And even if (the digital bank) fails, we chalk it up to a lesson learned and we move on and look for other ways to improve."

-1.png?width=2240&name=Banking%20Innovation%20Main%20page%20(2)-1.png "Banking Innovation Main page (2)-1")